Introduction

The global banking system plays a critical role in facilitating international trade, business transactions, and personal finance. With globalization increasing the interconnectivity of financial institutions, the need for secure and rapid cross-border transactions has never been more essential. One of the key pillars of international banking is the SWIFT (Society for Worldwide Interbank Financial Telecommunication) system.

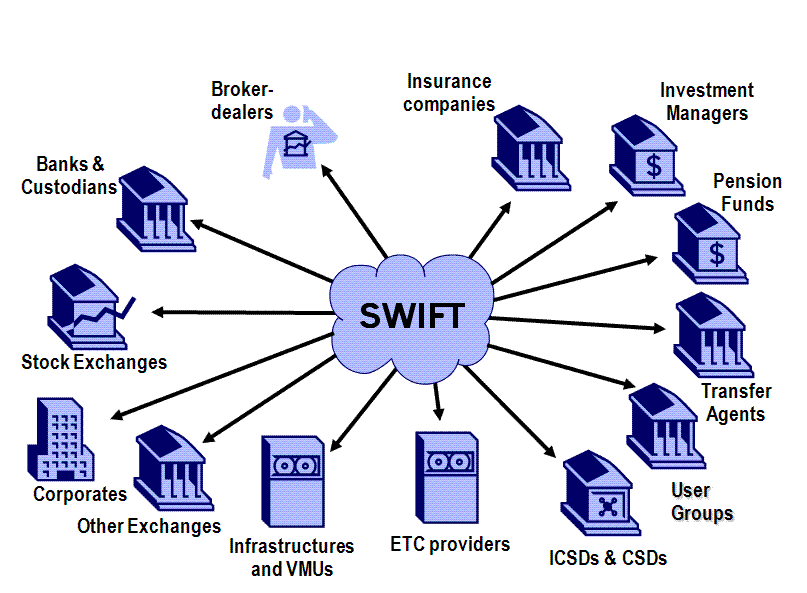

SWIFT serves as a standardized, secure messaging network that enables banks and financial institutions to communicate transaction-related information across borders efficiently. This system ensures that payments, trade confirmations, and securities transactions occur smoothly between institutions, regardless of location. Without SWIFT, international finance would be fragmented and inefficient.

Understanding SWIFT’s functions, security measures, and evolving landscape provides valuable insights into the global economy and the future of financial transactions. This article explores the inner workings of the SWIFT banking system, its impact on global finance, challenges, and what the future holds for this essential financial infrastructure.

Understanding the SWIFT Banking System

History and Evolution of SWIFT

SWIFT was established in 1973 in Belgium by 239 banks across 15 countries to create a unified, secure financial messaging system. Before SWIFT, financial institutions relied on telex messages, which were slow, prone to errors, and lacked a standard format for transactions. The launch of SWIFT revolutionized global finance by introducing a standardized, fast, and reliable communication network.

Over the decades, SWIFT has expanded its services to include compliance solutions, business intelligence tools, and payment innovations. Today, more than 11,000 financial institutions in over 200 countries utilize SWIFT, making it the backbone of international banking.

How SWIFT Operates

Contrary to popular belief, SWIFT does not transfer funds itself. Instead, it acts as a messaging network that securely transmits payment instructions between banks. A typical SWIFT transaction follows these steps:The sender’s bank sends a SWIFT message containing transaction details.

The message is securely transmitted through the SWIFT network to the recipient’s bank.

The recipient’s bank processes the payment based on the instructions.

Each participating bank has a unique SWIFT code (BIC – Bank Identifier Code), which ensures accuracy and efficiency in transactions.

The Functionality and Security of SWIFT

How Banks Use SWIFT for Transactions

SWIFT provides a standardized messaging framework that facilitates various financial operations, including:

International money transfers

Trade finance transactions

Securities trading and settlements

Foreign exchange operations

Banks and financial institutions rely on SWIFT’s efficiency to reduce delays, ensure compliance with international regulations, and enhance security.

Security Measures in SWIFT Transactions

Given the sensitive nature of financial communications, SWIFT employs multiple layers of security, including:

End-to-end encryption to prevent data breaches.

Two-factor authentication (2FA) for access control.

Real-time fraud detection and anomaly monitoring.

Regulatory compliance tools to prevent money laundering and financial crimes.

Despite these measures, SWIFT has faced cyberattacks in the past, prompting continuous enhancements in its security framework.

The Role of SWIFT in Global Finance

Facilitating Cross-Border Transactions

One of SWIFT’s primary roles is to enable seamless cross-border transactions. With its standardized messaging system, businesses and individuals can send money across continents efficiently. SWIFT ensures that payments are accurately processed, reducing errors and transaction failures.

Impact on International Trade and Economy

Without SWIFT, global trade would be severely impacted. Businesses rely on international banking networks to process payments for imports, exports, and investments. SWIFT enables international corporations, SMEs, and governments to conduct secure and rapid transactions, fostering economic growth.

Additionally, SWIFT plays a vital role in currency exchanges and remittances, ensuring that financial transactions occur within an efficient and standardized framework.

Comparison with Alternative Payment Systems

While SWIFT remains the dominant global financial network, new alternatives are emerging, including:

Blockchain-based systems such as RippleNet, offering decentralized, fast transactions.

Central Bank Digital Currencies (CBDCs), which could transform cross-border payments.

China’s Cross-Border Interbank Payment System (CIPS), providing an alternative for Chinese yuan transactions.

Despite competition, SWIFT continues to innovate by adopting ISO 20022 standards for improved transaction processing.

Challenges and Controversies in SWIFT Banking

Dependence on a Centralized Network

SWIFT’s centralized nature means that all transactions pass through a single system. While this ensures efficiency, it also poses risks such as:

System failures or downtimes affecting global transactions.

Vulnerability to cyberattacks, making it a target for hackers.

Geopolitical Implications and Sanctions

SWIFT is often influenced by international politics. Countries like Iran and Russia have faced SWIFT sanctions, restricting their access to the global financial system. Such exclusions have led some nations to explore alternative banking networks.

Cybersecurity Threats

Despite its security protocols, SWIFT has been targeted by cybercriminals. The Bangladesh Bank heist in 2016, where hackers attempted to steal $1 billion, highlighted vulnerabilities in the system. As a result, SWIFT has strengthened its cybersecurity measures.

The Future of SWIFT and Banking Innovations

Adoption of ISO 20022 Standards

SWIFT is transitioning to ISO 20022, a new global payment messaging standard that enhances data richness, efficiency, and security. This shift aims to improve interoperability among financial institutions.

Impact of AI and Automation

Artificial Intelligence (AI) is transforming SWIFT transactions through:

Real-time fraud detection

Automated compliance checks

Enhanced predictive analytics for financial flows

Rise of Digital Currencies and Decentralized Finance (DeFi)

The rise of cryptocurrencies and DeFi platforms presents both challenges and opportunities for SWIFT. While decentralized finance aims to reduce reliance on centralized networks, SWIFT is exploring integrations with blockchain technology to stay relevant in the digital era.

Conclusion

The SWIFT banking system remains a cornerstone of global finance, facilitating secure and efficient transactions worldwide. Despite emerging challenges, including cybersecurity threats and alternative payment networks, SWIFT continues to evolve by adopting advanced security measures and technological innovations.

As the financial industry transitions towards digital currencies, AI-driven automation, and blockchain-based transactions, SWIFT’s adaptability will determine its role in the future of banking. Whether it maintains dominance or integrates with new financial technologies, SWIFT’s legacy as a global financial facilitator remains unparalleled.

Frequently Asked Questions (FAQ

What is a SWIFT code, and why is it import nt? A SWIFT code is a unique identifier for banks used in international transactions to ensure accurate and secure money transfers.

How long does a SWIFT transfer take? Typically, SWIFT transactions take 1 to 5 business days, depending on banking procedures and intermediary banks.

Is SWIFT the same as a wire transfer? No. SWIFT is a messaging system, whereas wire transfers involve the actual movement of funds between banks.

Can individuals use SWIFT directly? No. SWIFT services are accessible only through banks and financial institutions.

Are there alternatives to SWIFT for global transactions? Yes, alternatives include RippleNet, China’s CIPS, and blockchain-based payment solutions.